As every first Saturday of each month, welcome to this month’s edition of the GasTurbineHub Newsletter!

In today’s newsletter:

📈 Retired jet engines into grid assets – A parallel turbine supply lane is forming.

🏭 Gas Turbine New Installations – Latest updates on projects and deployments.

⚙️ Gas Turbine Technology Developments – Innovations driving efficiency and performance.

🔥 Hydrogen Gas Turbines – Advancements in hydrogen-powered solutions.

📅 2026 Events Calendar – Upcoming industry events and opportunities to connect.

📣 Together With GasTurbineHub

GasTurbineHub Platform Pro (Igniter) is a professional intelligence layer designed for the global gas turbine community, bringing together three core resources in one platform:

-

A continuously updated Gas Turbine Calendar covering global conferences, workshops, user group meetings, and industry forums to support long-term planning;

-

An exclusive Gas Turbine Visuals library featuring high-quality, data-driven graphics translating complex technical, market, and policy developments into clear visuals for presentations and internal discussions;

-

And Gas Turbine Intelligence, delivering structured analysis that connects technology developments, market signals, and policy evolution into actionable insights for industry professionals and decision-makers.

You get a ton of access with a free account:

Let’s jump right in!

2026: When the unnormal becomes the new normal

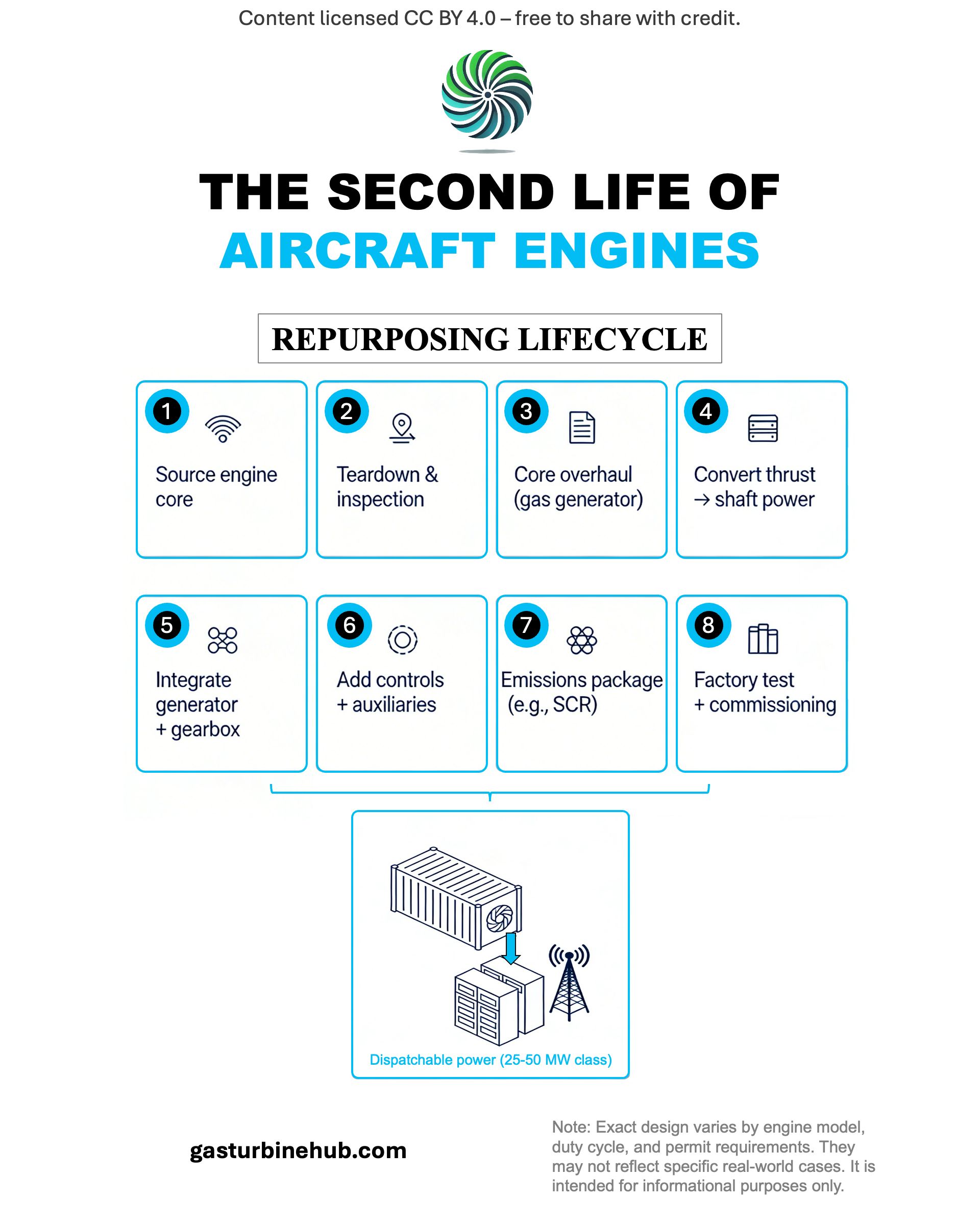

The gas-turbine market has a new, very unconventional entrant: retired aircraft engines, stripped off 747s and A320s, rebuilt as 25–50 MW power blocks for AI data centres and peaking duty. ProEnergy, Boom Supersonic and FTAI Power are turning a scrap stream into a parallel turbine supply chain, simply because the OEMs cannot deliver fast enough.

This is not a “cute workaround.” It is a structural response to a capacity-constrained turbine market meeting a data-centre-driven load shock, where time-to-power matters more than perfect heat rate. And it forces an uncomfortable question for the industry: if the fastest-growing buyers can source capacity outside the OEM funnel, what happens to the OEM’s control of the next installed base? The deeper implication is strategic, and it’s one we’ve repeated before: the real competition in gas turbines is not selling the next unit, it’s controlling the service funnel that follows it.

This article goes beyond describing an unusual technology pivot. It explains why repurposed flight engines are suddenly winning deals, how OEM backlogs and data-centre time-to-power have created a parallel supply lane and, more importantly, what this means for the real contest in our industry: not selling the turbine, but capturing the downstream service funnel (LTSA, parts, outage execution, and fleet data) that turns an installed base into a profit engine.

What this new market actually is

ProEnergy (PE6000): ProEnergy acquires CF6‑80C2 engine cores (originally used on aircraft including the Boeing 747) and retrofits them with aero-derivative components to operate as land-based gas turbines. The resulting PE6000 delivers up to 48 MW per turbine and is sold in two‑turbine blocks including generators, air cooling, SCR, and electrical balance-of-plant. ProEnergy says it has sold 21 turbines for two data-centre projects totaling more than 1 GW, explicitly designed as 5–7 year “bridging power” until grid interconnection arrives.

Boom Supersonic (Superpower): Boom is commercialising “Superpower,” a 42 MW natural-gas turbine derived from its supersonic engine technology, launching with Crusoe in 2027. Boom states Crusoe ordered 29 units totaling 1.21 GW, with an order book valued at over $1.25B. Boom raised $300M to build these turbines for Crusoe’s data-centre deployments, with deliveries starting in 2027.

FTAI Power (CFM56 conversions): FTAI is adapting the CFM56 platform into a 25 MW aeroderivative gas turbine for data centres facing multi-year delays in grid access, with production expected to begin in 2026. The premise is simple: use the world’s largest aircraft-engine ecosystem, hardware, spares, and MRO, to create a scalable alternative in a turbine market where conventional procurement is slow.

In other words: the market is building a “shadow OEM pathway” for the 20–60 MW segment, one that is fed by engine retirements and MRO capacity, not by new-turbine manufacturing slots.

Why this is emerging now

The industry already knows the first driver: lead times. OEM backlogs have extended into the second half of the decade, with delivery horizons now routinely quoted at six to seven years, and a new behaviour has re-emerged: paying reservation fees just to secure a place in the production queue. In that environment, the project that can start earning (or enabling revenue) in 12–24 months wins, even if it burns a little more fuel.

The second driver is the new offtaker: AI data centres. These buyers are not optimising around traditional utility planning cycles; they are optimising around compute deployment schedules and contractual uptime. Their grid problem is not theoretical, it is queues and timelines that do not match their business model, so they are bringing generation behind the meter.

The third driver is the overlooked asset pool: retirements. ProEnergy notes roughly 1,000 CF6‑80C2 engines are expected to retire over the next decade, creating a steady supply of cores for conversion. FTAI points to the sheer scale of the CFM56 universe (22,000+ produced) as the basis for a production-like conversion business rather than a boutique one.

Put these three together and the logic is brutally commercial: a repurposed-engine unit that is “available” can outperform a best-in-class turbine that is “unavailable”.

The hardware: what is actually being repurposed?

At the centre of this market are mature, high-volume aviation engines with deep MRO ecosystems:

-

CF6‑80C2 cores from wide-body fleets (e.g., 747-era platforms), converted into PE6000 units that deliver up to 48 MW each.

-

CFM56 engines from the 737/A320 era, adapted into 25 MW aeroderivative packages under FTAI Power.

-

Boom’s Superpower turbine, a new-build ground unit leveraging Boom’s supersonic-engine technology, marketed as a 42 MW natural-gas turbine.

This matters because it changes what “capacity” means. Capacity is no longer only what OEM factories can ship; it also becomes what the aviation retirement pipeline and conversion shops can process.

How this competes with traditional aeroderivatives

This is not a direct assault on H-class combined cycle. It is an attack on the fast-power wedge, the segment where aeroderivatives, small frames, and modular plants typically sit, and where buyers pay for speed and flexibility.

The conversion players compete on three non-negotiables:

-

Speed to site: ProEnergy argues a PE6000 can be delivered in 2027 by using retired cores, while OEM delivery timelines stretch toward 2029.

-

Modularity: Two-unit blocks, repeatable balance-of-plant, and redeployable assets fit the data-centre mindset.

-

Optionality: ProEnergy explicitly pitches redeployment, once grid power arrives, units can become backup, supplement utilities, or be sold onward.

The uncomfortable implication: OEMs may retain the premium end of the market, but lose a disproportionate share of the growth, because the growth is demanding speed more than perfection.

The hidden risk premium (including security)

This market is moving fast because it solves lead times, not because it eliminates risk. In practice, repurposed-flight-engine power plants introduce a different risk premium, mechanical, permitting, and security, that buyers, lenders, and insurers will increasingly price into contracts.

First, there is the reliability and maintainability question. Aeroderivatives excel at fast starts and cycling, but multi‑unit, behind‑the‑meter “baseload” service can shift the operating profile toward more frequent maintenance events and tighter spares discipline; the conversion player’s real product becomes fleet management, outage execution, and parts availability as much as it is heat rate.

Second, permitting and local acceptance are not automatic. Packaged jet‑engine units are compact and fast to deploy, but noise and emissions scrutiny near commercial campuses can become the schedule killer; compliance often hinges on add‑on pollution controls and site‑specific permit conditions, and those are rarely as “modular” as the hardware. We’ve seen this dynamic play out in real time around xAI’s “Colossus” data center in Memphis, where the use of multiple gas turbines triggered public controversy and regulatory scrutiny over permitting scope and air-emissions compliance.

Third, security deserves explicit diligence, and so does trust in the asset’s operating history. These packages rely on modern turbine controls and remote monitoring, which expands the cyber/OT attack surface if segmentation, vendor access, and patch governance are weak. Even behind‑the‑meter plants face physical security exposure because the generation and fuel interface become critical infrastructure for the data centre’s uptime. And unlike a factory‑new OEM unit with a clear delivery pedigree, repurposed cores introduce additional operator diligence around prior life, overhaul quality, records completeness, and residual risk, issues that can become a security-of-supply concern when your uptime depends on a multi‑unit fleet and a narrow spares ecosystem.

In short: the value proposition is real, but the diligence bar must rise.

What this means for stakeholders

OEMs: The risk is not near-term revenue (backlogs are full). The risk is strategic: a parallel installed base forming outside OEM manufacturing capacity and outside standard LTSA capture. If these fleets scale, they become their own services annuity, precisely where OEMs traditionally build long-cycle profit resilience.

Independent service providers and MROs: This is a growth lane. Conversion and lifecycle support are service-intensive, and the aviation MRO mindset – modules, exchanges, logistics – fits multi-unit power fleets well. But it also creates new “mini-OEMs” with vertically integrated models that can squeeze independent players unless they bring differentiated capability (controls, emissions, outage execution at scale).

Data-centre developers: They gain schedule control, but take on operational responsibility. Buying 1 GW of behind-the-meter gas is not just procurement, it is fuel strategy, permitting, O&M execution, and security governance.

Utilities and policymakers: In the near term, behind-the-meter generation can relieve grid bottlenecks. Over time, it can complicate planning and create a shadow capacity layer that sits outside traditional resource-adequacy logic.

Looking ahead

The near-term trajectory is clear: this market will expand as long as turbine lead times and interconnection timelines remain mismatched to AI deployment. The more interesting question is what happens when OEM capacity catches up.

Our view: even if OEM lead times normalise later this decade, the “used engine → power” lane is likely to persist for at least three reasons:

-

A mature ecosystem will exist (conversion lines, spares pipelines, operating playbooks, financiers familiar with the assets).

-

Buyers will have learned that modular aeroderivative blocks can be deployed, redeployed, and monetised with a flexibility that large frames cannot match.

-

OEMs may not want to fully compete on this segment’s economics if it dilutes margins, leaving room for specialists.

But the lane has a ceiling. Feedstock is finite, duty profiles can be unforgiving, and permitting/security standards will tighten as these units move from “temporary bridge” to “normal infrastructure.” The winners will be the players who treat this not as hardware arbitrage, but as a full-stack lifecycle business.

References: ProEnergy PE6000, Boom Supersonic Power, FTAI Power, Mexico Business News. (2025, Nov 4). “ProEnergy Converts Boeing 747 Engines to Power AI Data Centers.”, TechCrunch. (2025, Dec 8). “Boom Supersonic raises $300M to build natural gas turbines for Crusoe data centers.”, ePlaneAI. (2025, Dec 29). “FTAI Aviation introduces platform to convert CFM56 engines into power turbines.”, AviTrader. (2026, Jan 1). “FTAI unveils CFM56 Power platform.”, Distribution Strategy. (2026, Jan 1). “FTAI Aviation Moves into Data Center Power, Leveraging Engine Distribution and MRO Platform.”

Join the conversation: Sign up for our newsletter to stay updated on developments in gas turbine technology and the energy sector.

The Latest News in a Snapshot

Intelligence and Insights Reports – Stay ahead

|

|

Gas Turbine New Installations

-

Doosan Enerbility wins KOSPO order for three 380 MW K‑gas turbines

“Doosan Enerbility and KOSPO agreed to install three domestically developed 380 MW‑class gas turbines at the new Hadong CCPP (2 units) and Goyang Changneung CHP (1 unit), totaling about 1,500 MW, with commercial operation targeted for December 2029.“

Source: Doosan (11 February, 2026) -

Fort Martin 1,200 MW CCGT application filed in West Virginia

“Monongahela Power and Potomac Edison applied to the West Virginia PSC to construct a 1,200 MW combined‑cycle gas plant at the Fort Martin Power Station site, with estimated cost US$2.84 billion and targeted commercial operation in late 2031, to address projected capacity shortfalls.“

Source: PSC (14 February, 2026) -

Lincoln Electric System orders two LM6000VELOX units

“GE Vernova will supply two LM6000VELOX aeroderivative gas turbine packages for LES’s Terry Bundy plant, adding ~100 MW of fast‑start, flexible capacity by 2029 to support growing demand in Lincoln, Nebraska.“

Source: GE Vernova (16 February, 2026) -

Serbia–Azerbaijan deal for 500 MW CCGT near Niš

“Serbia and Azerbaijan signed an intergovernmental agreement to build and operate a ~500 MW combined‑cycle gas‑fired plant near Niš (≈350 MW electricity, 150 MW heat), using Azeri gas and representing a €600 million investment, with construction expected to take just over two years.“

Source: Balkan Green Energy News (16 February, 2026) -

Abuja 350 MW gas power plant progresses in Nigeria

“The power plant being constructed by NNPC, which will be powered by gas from the Ajaokuta–Kaduna–Kano (AKK) Gas Pipeline, which is expected to deliver 350MW under Phase One of the project.“

Source: FNG Power Company (19 February, 2026) -

Blackstone completes Magnolia 694 MW CCGT in Louisiana

“Blackstone’s Magnolia Power Generating Station, a 694 MW GE 7HA.03‑based CCGT in Plaquemine, Louisiana, reached commercial operation in late February 2026, providing power for over 500,000 homes and completing construction that began in 2022.“

Source: Power Magazine (28 February, 2026)

Gas Turbine Technology and Market Developments

-

Xcel Energy reserves five F‑class gas turbines via alliance with GE Vernova

“Xcel Energy’s February 2026 strategic alliance with GE Vernova includes purchasing five additional F‑class gas turbines and reserving manufacturing capacity for multiple GW of wind, aiming to support up to 6 GW of new large‑load (mainly data center) demand across its territories.“

Source: Xcel Energy (03 February, 2026) -

Fermi America announces arrival of six Siemens SGT‑800 gas turbines at Port of Houston

“Fermi America reports the arrival of six Siemens Energy SGT‑800 gas turbines and generators for its Project Matador energy campus, marking a major logistics milestone and providing roughly one‑third of the first gigawatt of campus capacity.“

Source: Fermi America (09 February, 2026) -

GT26 HE upgrade highlighted at Coryton power station

“GE Vernova reports successful GT26 High Efficiency upgrade at Coryton CCGT, with advanced turbine, compressor and combustor hardware delivering higher output, better efficiency and extended inspection intervals while lowering CO₂ intensity.“

Source: GE Vernova (9 February, 2026) -

Siemens Energy Q1 FY 2026 earnings show record gas‑turbine orders

“Siemens Energy reports its strongest Gas Services quarter ever, booking orders for 102 gas turbines, with 40% of orders from the U.S. and 35% from Europe, underscoring surging global demand.“

Source: Siemens Energy (11 February, 2026) -

Entergy Texas issues 2026 CCCT RFP

“Entergy Texas launches a 2026 RFP seeking new gas‑fired combined‑cycle combustion turbine capacity from 2032 or earlier, targeting around 1 GW of projected load growth and evaluating potential new CCCT plant development in its territory.“

Source: Entergy Texas (12 February, 2026) -

Trump‑backed 9.2 GW gas plant proposed in Ohio

“President Donald Trump has introduced a $33 billion agreement with Japan to develop a 9.2 gigawatt gas-fired power project in Ohio, a proposal that could rank as the largest of its kind in the US if completed, but several core elements are still taking shape.“

Source: TradingView (20 February, 2026) -

Ansaldo Energia to upgrade Thisvi CCGT gas turbine

“Ansaldo secures a contract to upgrade the AE94.3A gas turbine at the Thisvi CCGT plant in Greece, increasing output, efficiency, ramp rate and reducing CO₂ emissions under a renewed long‑term service agreement.“

Source: Ansaldo Energia (26 February, 2026) -

Entergy Texas issues 2026 CCCT RFP

“Entergy Texas launches a 2026 RFP seeking new gas‑fired combined‑cycle combustion turbine capacity from 2032 or earlier, targeting around 1 GW of projected load growth and evaluating potential new CCCT plant development in its territory.“

Source: Entergy Texas (12 February, 2026)

Gas Turbine Decarbonisation News

-

KIT achieves runtime record with compressorless hydrogen gas turbine

“KIT researchers run a compressorless hydrogen gas turbine for 303 seconds, surpassing NASA’s 250‑second benchmark, using pressure‑gain combustion to eliminate mechanical compression and achieve first electricity generation with this concept.“

Source: Hydrogen Central (18 February, 2026)

Gas Turbine Related Events Happening in March

This month’s events are just a snapshot.

Explore more than 30 upcoming gas turbine conferences, exhibitions and user group meetings on GasTurbineHub.

FT4/FT8 User Group Meeting 2026

Date: March 17–19, 2026

Location: Charlotte, New Carolina (In-person)

Organizer: FT4/FT8 Steering Committee

Website: https://gasturbinehub.com/event/ft4-user-group-meeting-2026/

22nd ETN Global Annual General Meeting & Workshop

Date: March 23–25, 2026

Location: Malmö, Sweden (In-person)

Organizer: ETN Global

Website: https://gasturbinehub.com/event/22nd-etn-global-annual-general-meeting-workshop/

10th EPRI European Workshop Week 2026

Date: March 23–26, 2026

Location: Prague, Czech Republic (In-person)

Organizer: EPRI

Website: https://gasturbinehub.com/event/10th-epri-european-workshop-week-2026/